Taxes

2023 Budget and municipal taxes brochure (See starting page 4)

Property assessment rolls website

| 2024 payment of municipal taxes | |

| First instalment: | February 5, 2024 |

| Second instalment : | May 27, 2024 |

Online taxation, billing and collection (TFP) services for property owners

Don’t forget to change your preferences to receive communications in English.

Access to online services

Services provided

Registration grants you access to the following services:

- Access the various documents received electronically

- Access your balance and statement of account

- Receive a reminder by email for the second instalment

- Modify your access data

- Modify your property selections to subscribe or unsubscribe from electronic document services

Registration to the electronic document service

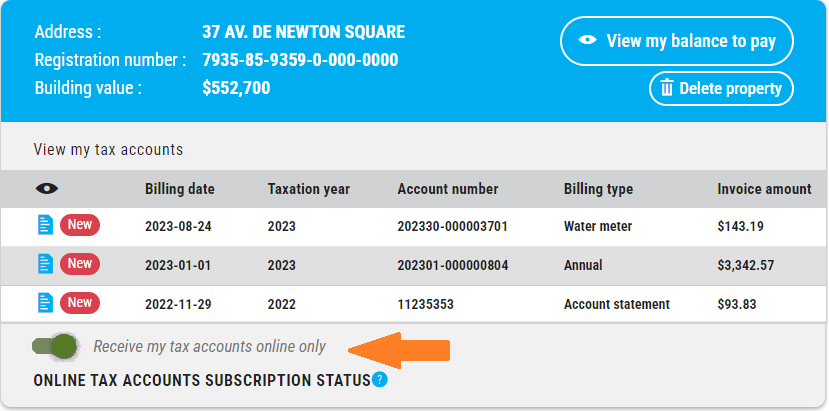

You can also subscribe to the electronic document service, you will be notified by email when a new document is available in your account. When you register for this service, you no longer receive paper invoices. To do so, you must confirm “Receive my tax accounts online only” as illustrated below.

Registration is done directly on the Voilà! platform.

To register for online services :

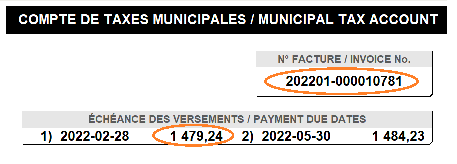

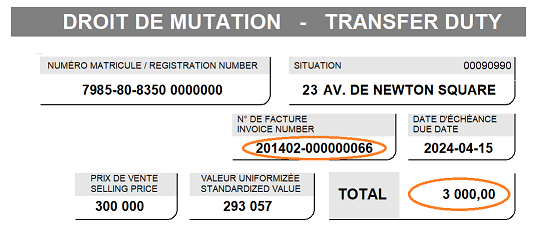

| Have one of the following documents ready: tax bill or deed. | |

| CURRENT OWNERS | NEW OWNERS |

| To proceed, you will need the invoice number of the last municipal tax bill issued and the amount of the first instalment. | To proceed, you will need the transfer tax (“welcome tax”) invoice number (if you have just taken possession of a property) and the invoice amount. |

|

|

Complete the form :

Once you have completed the registration, you will receive an email confirming your registration.

For more information, contact the taxation team at 514-630-1300, extension 1829.

Access to the taxation roll for residents

To view the taxation roll or the property tax bills for an address, click here.

Notary and commercial account access

Notice to notaries:

- You must inform the new owner(s) of the dates of upcoming payments and the amounts to be paid.

- You must adjust the water used by the seller in the same way as the tax distribution, regardless of the property. Please fill out the Water meter adjustment request.

Commercial and professional access – Online services

Services available

- View the taxation roll and property tax bills for an address

- View the tax account statements for a building

For professional access, the cost per consultation is $50 (plus taxes). Please note that future consultations for the same property will be free of charge until 30 days following the first consultation.

Current rates

2024 Tax rates per $100 of assessment

| Vacant land | $1.2522 |

| Residential building | $0.6261 |

| Residential building with 6 or more dwellings | $0.6261 |

| Commercial building (first $1M) | $3.0651 |

| Commercial building (portion above $1M) | $3.4605 |

| Industrial property | $2.6270 |

Water Tax

| Per cubic metre | $1.2210 |

| Residential buildings | Billed once a year |

| Non-residential and Industrial Property | Billed twice a year |

Water Meter Rental – Annual Rates

Based on size of meter in inches

| ½” or ⅝” or ¾” | $12 |

| 1″ or 1¼” | $37 |

| 1½” | $81 |

| 2″ | $160 |

| 3″ | $210 |

| 4″ | $410 |

| 6″ or more | $655 |

How to pay your various tax bills

There are a number of ways available to pay your municipal tax bill, transfer tax bill or water tax bill.

- through a financial institution: in person, by phone, via the Internet or at an ATM (allow two business days for the transaction to be processed by the financial institution). The same “Reference number for electronic payment” must be used for payment of municipal taxes, transfer duties and water bills.

Major financial institutions that accept online payment

CIBC Bank

Laurentian Bank of Canada

National Bank of Canada

Royal Bank of Canada

TD Canada Trust

Caisses populaires Desjardins

- by signing up for the pre-authorized payment method offered by the City (for your municipal tax bill only).

- by cheque or money order payable to the City of Pointe-Claire (allow a delivery time of three business days).

- in person, at the City Hall tax counter: by Interac debit, by cheque (allow three business days before the due date) or in cash.

Pre-authorized payments (PAP)

You can sign up for pre-authorized payments.

This is a simple, effective way to meet the deadlines and avoid late fees.

When you sign up for the pre-authorized payment plan, each payment is taken right from your bank account. If you remain the owner and your banking information does not change, renewing is not required. However, you must inform the City of any changes, including the sale of your property.

Two pre-authorized payment plans are offered:

- By due date (according to you tax bill)

- Monthly* (12 payments – if your tax bill is more than $300)

*Monthly payments enable you to spread your payments out over 12 months from February to January of the following year. However, interest and penalty charges are calculated on balances due after the two legal deadlines.

The first year, the City Hall tax counter staff will let you know the amount of the monthly payment, including interest and penalty charges. After that, the amount of your monthly payment will be indicated on your tax bill.

Procedure

To register for one of the pre-authorized payment plans:

- download the Registration Request form or pick one up at the City Hall tax counter at 451 Saint-Jean Blvd.

- fill out the required fields

- submit your completed form to City Hall, along with a cheque specimen, 10 business days before the deadline or the payment withdrawal date

How to cancel the registration

Download the required form or pick one up at the City Hall tax counter at 451 Saint-Jean Blvd. Then send it to the following address:

Tax Counter

451 Saint-Jean Blvd.

Pointe-Claire QC H9R 3J3

Your request will be processed within ten business days after the form is received.

How to modify the registration

- fill out the registration request form

- check the modification box

- Send your completed form, along with a cheque specimen, to the following address:

Tax Counter

451 Saint-Jean Blvd.

Pointe-Claire QC H9R 3J3

Your request will be processed within ten business days after the form is received.

Transfer tax (welcome tax)

Taxes on transfers of immovables are amounts that are payable when the right of ownership on a property is transferred. It is the property buyer who is responsible for paying those taxes. If there are multiple buyers, they are jointly and severally responsible for paying those taxes.

All municipalities are required to collect a transfer tax whenever a property within their territory is transferred. (Act respecting duties on transfers of immovables, CQLR c. D-15-1)

The property transfer tax is charged when a property is purchased; it is payable in a single instalment.

When a property is transferred, the City of Pointe-Claire does not automatically re-issue property tax bills. It is the new owner’s responsibility to ensure that the municipal taxes due are paid.

- Basis of imposition

- Comparison factor

- Calculation of the tax on property transfers

- New! Legislative changes

- Exemption

- Special duties

Basis of imposition

The basis of imposition is the greatest of the following three amounts:

- The amount actually paid for the transfer of the immovable (not including GST and QST)

- The amount of the consideration stipulated for the transfer of the immovable (generally the amount shown on the deed of sale)

- The amount of the market value of the immovable at the time of its transfer (value entered on the property assessment role multiplied by the comparison factor of the transfer’s fiscal year)

The following are generally regarded as considerations:

- the value of any property furnished at the time of the transfer

- the price indicated in the contract

- privileges, mortgages or other charges encumbering the immovable

Comparison factor

If the imposition is done on the basis of the market value at the time of the transfer, the value entered on the property assessment role must be multiplied by the comparison factor of the transfer’s fiscal year.

The comparison factors of the City of Pointe-Claire for the following fiscal years are:

| Fiscal year | Comparison factor |

| 2022 | 1.18 |

| 2023 | 1.00 |

| 2024 | 1.10 |

Calculation of the tax on transfers of immovables

The tax is calculated as follows:

| On that portion of the basis of imposition | Rate |

| That does not exceed $58,900 | 0.5% |

| That exceeds $58,900 but does not exceed $294,600 | 1% |

| That exceeds $294,600 but does not exceed $500,000 | 1.5% |

| That exceeds $500,00 but does not exceed $1,000,000 | 2% |

| That exceeds $1,000,000 | 2.5% |

Here is a sample calculation using $726,000 as a basis of imposition:

| Multiply $58,900 by 0.5% | = | $294.50 |

| Then multiply $235,700 by 1% | = | $2,357 |

| Then multiply $205,400 by 1.5% | = | $3,081 |

| Then multiply $226,000 by 2% | = | $4,520 |

| So, for a basis of imposition of $726,000, total duties will be | : | $10,252.50 |

Amendments to the Act respecting duties on transfers of immovables

On March 18, 2016, the day after the speech on the 2016-2017 Budget by the provincial Minister of Finance, various legislative amendments to the Act respecting duties on transfers of immovables concerning the following aspects came into effect:

- exemptions on transfers between separated common-law spouses;

- exemptions on transfers between closely related legal persons;

- exemptions on transfers between a natural person and a legal person;

- implementation of a mechanism for disclosure of share transfers;

- implementation of a mechanism for disclosure of property transfers that are not registered at the Registry Office;

- exemptions on transfers involving international organizations.

For more information on these amendments, we encourage you to read the 2016-2017 Budget by visiting the following website: budget.finances.gouv.qc.ca/index_en.asp.

Taxpayers who are required to disclose share transfers or transfers of immovables can contact us at the following email address: taxes@pointe-claire.ca.

Disclosure forms:

- Transfer of immovables disclosure (hyperlink to form)

- Exemption disclosure (hyperlink to form)

Exemption

A buyer may be exempt from paying the duties on a transfer in certain cases as set out in the Act respecting duties on transfers of immovables CQLR, c. D-15.1. The notary must enter a statement in the deed of sale (or instrument of transfer) so that the buyer receives the exemption from the transfer duty as per the cases provided for in the legislation.

Main situations justifying an exemption:

- Transfer to a direct ascendant or descendant (sale from father to son; from grandmother to granddaughter);

- Where the transferor is a natural person and the transferee is a legal person where 90% of his/her issued shares having full voting rights are owned by the transferor;

- Transfer between married couples or between common-law spouses (as defined in the Act respecting duties on transfers of immovables). Same-sex partners are included in the provisions of the law.

Note that, since March 18, 2016, common-law spouses separated by reason of the breakdown of their union have 12 months from the date of separation to complete the transfer, otherwise the exemption will not be applied. Married couples have 31 days after the divorce judgment to complete the transfer if the divorce judgement does not award one of the spouses ownership of the immovable.

Several other situations justifying exemption are provided for by the Act.

Special duties

Special duties are a form of compensation in lieu of transfer duties that are billed to buyers whose transaction is exempted.

The Act respecting duties on transfers of immovables – CQLR c. D-15.1 sets the amount of the special duties based on the transferred values:

| Value of the property | Amount payable |

| Immovable of less than $5,000 | No duties |

| Immovable of $5,000 to less than $40,000 | Special duties equivalent to the transfer duties (0.5%) |

| Immovable of $40,000 or more | $200 |

Property assessment roll

The property assessment roll will be in force for the years 2023 to 2025 inclusive. Unless your property has undergone significant structural changes, its value will remain unchanged during this period.

The City of Montréal’s Direction de l’évaluation foncière is responsible for the property assessment roll. The value of your property is equivalent to its most likely selling price in a free and competitive market.

You can consult your property’s assessment value in more detail on the City of Montréal’s Direction de l’évaluation foncière website or by going in person to one of the regional offices of the Direction de l’évaluation foncière:

- 1868 des Sources Blvd., Suite 500

Pointe-Claire QC H9R 5R2 - 255 Crémazie Blvd. E., Suite 600

Montréal QC H2M 1M2

Downloads

Procedure – Application for review of the property assessment roll

Form – Application for review of the property assessment roll

Sale of immovables for unpaid taxes

Information

514-630-1300, extension1829, taxes@pointe-claire.ca